Ready to get started?

If you’re ready to start planning for a brighter financial future, Rockbridge is ready with the advice you need to achieve your goals.

October 21, 2019

AllInvestingNews

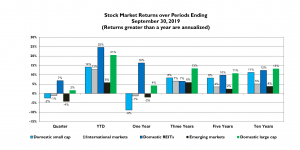

It was generally an off quarter for stocks, except for Real Estate Investment Trusts (REITs). The year-to-date numbers look good. Recent periods show variability among individual markets as well as within various time periods – REITs continue to do well, no doubt reflecting declining interest rates. One theme running throughout the past ten years’ stock returns is the better-than-average numbers for domestic stocks versus international stocks. While this behavior is clear by looking back, investment decisions are made by looking ahead. Markets have no memory so we can’t bank on superior results from domestic markets continuing.

Another theme in these ten-year numbers is that the domestic large-cap market (S&P 500) returns consistently exceeded those of other benchmarks. Expected earnings and growth drive stock returns, and any surprises that alter these expectations produce volatility. S&P 500 stocks are well-followed by analysts; there is no reason to think that they will consistently provide positive surprises. So, what’s going on? It may be simply that S&P 500 stocks are the default investment when investors desire more risk in the face of anemic returns in other markets. These results are by and large unrelated to company earnings and investments opportunities – suggesting a “passive management bubble”. If that explains some of what is happening, then the relative results in this market won’t go on forever.

We know that maintaining a globally diversified stock portfolio has the best chance for long-term success. However, because domestic markets, especially the S&P 500, are so popular and familiar, it has been especially difficult for investors to maintain strategic commitments among several other markets this time around.

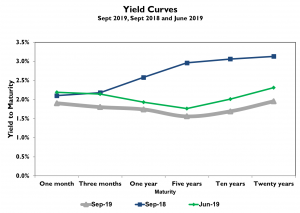

A yield is what you earn by holding a bond to its maturity. Changes in yields drive returns – falling yields are positive; rising yields negative. The longer a bond’s maturity, the greater the impact a given change will have on prices and returns.

The Yield Curve is a picture of how these yields vary across several bond maturities. Shown to the right are U.S. Treasury securities a year ago (September 2018), at the end of last quarter (June 2019) and today. Not only can changes help us better understand bond returns, they can also be useful predictors of the direction of interest rates. The sharp fall-off over the past year means positive bond returns, especially at the longer end – the long-term Treasury benchmark (7-10 yrs.) earned nearly 10% while the short-term benchmark (1-3 yrs. Treasury) earned only 3%. Bond returns were positive over the past quarter reflecting the downward shift in the Yield Curve.

Last year’s curve is typical; the more or less “flat” curve we see today is not. However, it is consistent with expected lower rates in the future. The story behind this prediction is that the Fed will continue to reduce rates to fight the upcoming economic decline. However, while there is some indication of a slowdown, neither the stock market, nor labor markets (where unemployment is at historical lows) seem to anticipate much of a slowdown. The recent cut in interest rates is more in response to political pressure – at these levels the effect of any decrease will be mostly perception.

There is a lot of noise about a coming recession. While the numbers still look reasonable, the tools to respond may not be as potent this time around. The hue and cry for the Fed to reduce interest rates notwithstanding, and with rates at historically low levels and massive Treasury securities on the Fed’s balance sheet, there is not much room for monetary policy to make a difference. As far as fiscal policy is concerned, the Government is already running substantial deficits due to the recent tax cut. The positive impact may be behind us and with today’s political dysfunction, the opportunity to do more with fiscal policy may not be available. A lot of uncertainty – little wonder the stock market is volatile. With the large tax cuts in place and an accommodative Fed, we have enjoyed a nice ten years that may be difficult to repeat.

If you’re ready to start planning for a brighter financial future, Rockbridge is ready with the advice you need to achieve your goals.