Ready to get started?

If you’re ready to start planning for a brighter financial future, Rockbridge is ready with the advice you need to achieve your goals.

April 21, 2017

InvestingNews

On March 15, 2017, the Federal Reserve increased interest rates for just the third time since the financial crisis in 2008-2009. Investment theory tells us when interest rates rise, bond prices fall, so rising interest rates are bad for bond returns. However, bonds have performed well since the Fed raised rates a few weeks ago… WHY?

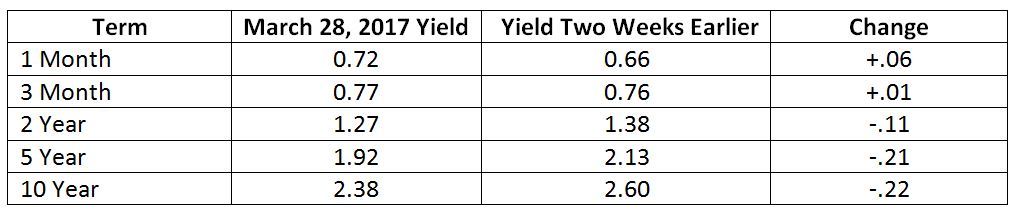

Looking closer, we see that most interest rates fell after the Fed raised rates:

Fed Controls Short End of the Curve

If you plot this data on a graph, you will see the yield curve – an upward sloping line that shows higher rates for longer maturities. When the Fed raised rates, the curve “flattened,” meaning short-term rates rose slightly while long-term rates dropped slightly. The yield curve is constantly changing shape, and is not always upward sloping – it is referred to as inverted when short-term rates are higher than long-term rates.

Markets Anticipate

The Fed raised rates by 0.25% and the one-month treasury rate went up 0.06% because everybody knew that the Fed was planning to raise rates; the change was already factored in almost entirely. There was some small chance the increase would be delayed, so there was still room for a small increase when the change became certain.

Inflation Expectations Drive Long-Term Rates

What markets did not anticipate was a Trump Presidency, so there was a significant jump in longer-term rates immediately following the Election last Fall. Inflation expectations drive long rates, and President Trump’s proposals to cut taxes and spend billions on infrastructure are perceived as inflationary. Inflation happens when there are too many dollars chasing too few goods, and prices rise.

Monetary Policy

Theory suggests that cheap money promotes economic growth, which creates more jobs. However, as the economy approaches capacity and full employment, demand for goods and services exceeds supply; the result is unwanted inflation. The mission of the Federal Reserve is to maintain the ideal equilibrium between full employment and price stability through monetary policy.

If the Fed is too slow to raise rates and cool down rapid economic expansion, the market can push long-term rates up in anticipation of higher inflation. This is driven by the fact that investors want an interest return that exceeds inflation and compensates them for taking risk. So even if risk stays the same, they demand a higher rate when inflation expectations rise.

In the current economy the opposite seems to be true. The market is concerned that any increase in rates will dampen an already sluggish economy, putting even less pressure on rising prices. So the Fed raised rates… but interest rates went down.

Conclusion

It is important to remember, as recent events illustrate, bond returns are not directly impacted by the Fed Funds Rate. Through monetary policy the Fed can influence economic growth, and inflation expectations, but the linkage is not very solid. In the aftermath of the financial crisis they were left “pushing a string” – the Fed Funds Rate went to zero, they pumped up money supply, and economic growth and employment still collapsed. Similarly in today’s economy, monetary policy may be important, but its impact can be easily overshadowed by fiscal policy (taxes and government spending). The bottom line – Do not necessarily assume that bond returns will suffer every time the Fed raises rates.

If you’re ready to start planning for a brighter financial future, Rockbridge is ready with the advice you need to achieve your goals.