Ready to get started?

If you’re ready to start planning for a brighter financial future, Rockbridge is ready with the advice you need to achieve your goals.

July 3, 2019

AllInvestingRetirement

Target date funds have become some of the most common investments in America. Not coincidentally, their rise in prevalence has coincided with 401(k)s gaining in popularity. We have seen it here locally; many of the largest employers in Syracuse (Syracuse University, Carrier, Lockheed Martin, General Electric, Welch Allyn, and Niagara Mohawk/National Grid) had pensions. In almost all cases, the pension has been frozen and replaced with a 401(k)s that provides a target date fund (often the default investment when an employee enrolls).

Target date funds are good investments, they achieve two important goals to help satisfy the fiduciary obligation of the 401(k) plan’s advisor:

Diversification: They are generally diversified over thousands of stocks and bonds incorporating multiple asset classes.

Simplification: Target date funds are logistically simple. You only need one holding and it automatically adjusts your allocation from being aggressive when you are young to more conservative as you near retirement.

In most 401(k) plans which have automatic enrollment (73% of plans are now set up for automatic enrollment), target date retirement funds are the default investment. This means without any action taken, you’ll be investing in your 401(k), and it will be through a target date fund based on your age. Generally, you are placed in the target date fund closest to when you’ll turn 65, regardless of whether you plan on retiring at 55 or 75.

It is important to understand not all target date funds are the same, they can vary in allocation and cost.

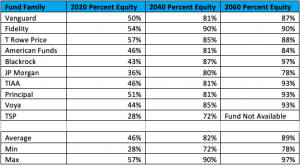

In terms of allocation, the most famous instance of allocation discrepancy was in 2008. During that year, returns on 2010 target date funds (designed for those retiring in two years) varied from -3.5% to -41.3%. Since then, companies managing target date funds have more standardized their allocations, but differences still exist. The following chart shows the stock allocation for different target date funds of various companies or organizations.

The largest disparity is in funds close to retirement. Federal Employees invested in the Thrift Savings Plan (TSP) who have chosen the Lifecycle Funds will have a very heavy allocation towards bonds as they near retirement. However, those who are invested with T. Rowe Price (common for employees at Syracuse University), are close to 60% equities despite being invested in the exact same fund year. In 2008, the TSP’s 2010 fund would have lost about 6% while the allocation held by T. Rowe Price would have dropped 20%. This is not to say the T. Rowe Price allocation is too risky, but rather a reminder that it’s important to understand exactly how your funds are invested.

While not a 30% disparity, we still see decent differences in the allocation of 2040 target date funds. Fidelity comes in most aggressive with a 90% equity allocation – that’s a lot of stock market risk for someone who is 45, especially if they plan on retiring in their 50s.

For 2060 target date funds, we see Blackrock has an effective all equity allocation while JP Morgan inexplicably has a more conservative allocation than their 2040 fund, with 15% in bonds and 7% in money market funds.

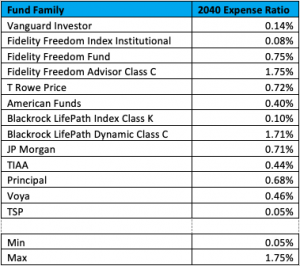

Another discrepancy between target date funds is cost. The following table shows the expense ratios associated with each 2040 target date fund.

The expense ratios of target date funds are confusing if you work in the industry. If you work outside the industry, good luck. Fidelity, the largest custodian of 401(k)s in the country, is a perfect example. The average investor would assume they are in Fidelity’s 2040 Target Date Fund. But Fidelity alone has 21 different 2040 Target Date funds. The expense ratios of these funds range from 0.08% to 1.75% despite more or less doing the same thing. This price complexity comes from two things:

Multiple Series: The largest fund companies have many series for the same type of investment. Fidelity, Blackrock, and Schwab all have actively managed target date funds that charge high fees and low-cost non-active target date funds. Look for the word index as that is usually low-cost.

Different Share Classes: Clients of Rockbridge don’t have to worry about share classes because they are associated with commissions. As fee-only fiduciary advisors, we are prohibited from receiving a commission on a product we recommend, but some 401(k)s will have commission-based investment options. Even among choices that don’t receive a commission, you can have difference expense ratios. Fidelity’s Advisor Freedom series has an “Institutional” share class which costs 0.75%, a “Z” share class which costs 0.65% and a “Z6” share class which costs 0.50%.

We’ve found investors can sometimes get the same exposure as the more expensive target date fund options through the use of low-cost funds within the same 401(k) plan. Saab Sensis, a successful local employer uses a lineup which includes Principal as their target date fund family. These target date funds charge from 0.57% to 0.79% depending on the year. However, they offer lower cost mutual funds which can get the same exposure for around 0.25%, leading to substantial savings for the investor.

Lockheed Martin is similar. Most of their target date fund options cost 0.54%, but you can get the same exposure through individual index funds for 0.08%.

In conclusion, target date funds are generally good investments, but it’s important to know exactly what your getting in terms of allocation and cost. As always, if you have questions or concerns, please contact your advisor at Rockbridge and we can help look through your specific situation as it relates to target date funds or more general financial planning.

If you’re ready to start planning for a brighter financial future, Rockbridge is ready with the advice you need to achieve your goals.