Ready to get started?

If you’re ready to start planning for a brighter financial future, Rockbridge is ready with the advice you need to achieve your goals.

April 14, 2016

AllInvestingNews

Stock Markets

After January’s rough start, stock markets bounced back nicely in March, bringing most numbers into the black for the quarter. Domestic Small Cap and International Developed Markets are the exception – down about 1.5% and 2%, respectively. Notice from the accompanying chart that it was Emerging Markets that led the way, earning nearly 8% for the quarter. While not nearly enough to bring longer-period returns into the black, it does give some sense of how diversification works.

The uptick in stock returns in March seems to reflect a more or less positive resolution to some of the recent economic uncertainty – commodity prices have rebounded, figures from China appear better than expected and the domestic economy shows signs of continued improvement with fourth quarter GDP numbers revised upwards. Also, markets have calmed down a bit – daily volatility of the S&P 500 is below average in March.

While certainly dominating the airwaves, markets don’t seem to be paying much attention to the goings on in the Presidential election. Don’t let expected political environment cloud investment decisions – assessing not only the probability, but also the impact of the eventual election of any of the current contenders, is tricky indeed.

Market prices are based on the future – today’s prices reflect a set of expectations, which may or may not be realized. Prices are set expecting a positive return. The possibility for short-run losses, while not expected, is risk. It’s what we endure to earn the long-run positive returns. For sure, however, there will be lots of unpredictable ups and downs along the way as the markets digest the news of the day.

Bond Markets

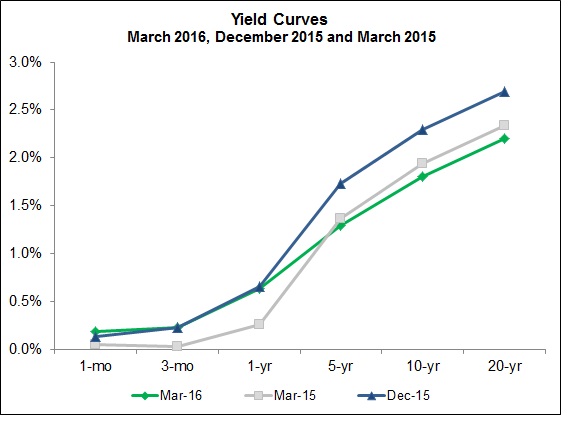

The yield on the bellwether 10-year U.S. Treasury security fell about 0.5% to 1.8% by the end of the quarter reflecting positive returns in Domestic Bond Markets. Note the changes in the accompany Yield Curves chart – short-term rates increasing due to the Fed’s tightening, yet rates over longer periods falling. The Fed can impact short-term rates; the market sets longer-term rates.

We are in the midst of an environment of historically low interest rates. In fact, as a component of current monetary policy, the Central Banks of Japan and some European countries have begun to charge member banks a negative interest rate to hold reserves. Also, the market determined rate on five-year inflation protected U.S. Treasury securities is a negative 0.3%. Yields on the ten-year security have fallen to under 1.8%, which if inflation over the next ten years is expected to exceed 2%, also produces a negative yield.

While this interest rate environment has persisted for some time, markets can be out of whack for extended periods. However, expected deflation over longer periods could make negative yields rational. Still, I would be hard pressed to argue that negative interest rates are the “new normal” and are here to stay. Negative interest rates can’t go on forever, and Stein’s Law (Herbert Stein, Chairman of the Council of Economic Advisors in the Nixon and Ford Administrations) tells us that “If something can’t go on forever, it will stop.”

If you’re ready to start planning for a brighter financial future, Rockbridge is ready with the advice you need to achieve your goals.