Ready to get started?

If you’re ready to start planning for a brighter financial future, Rockbridge is ready with the advice you need to achieve your goals.

April 10, 2015

All

Stock Markets

Stock Markets

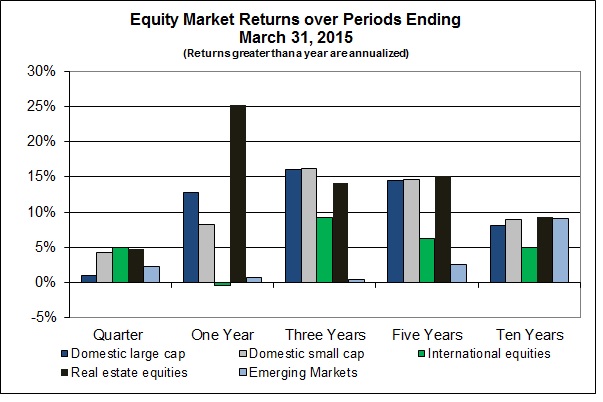

After a lot of bumps and bruises, as we show in the accompanying chart, stocks markets were up across the board over the March quarter. Although lagging over longer periods, international developed markets led the way this quarter.

Look at the returns from emerging markets. While the 10-year results are consistent with other markets, returns are well below in other periods. I think this simply reflects the unsustainability of the early-on exuberance shown by investors for the BRICs (Brazil, Russia, India and China). In any market or market segment, sustained periods above or below long-term averages generally don’t last.

The latest moves in market averages seem to be in response to comments from pundits observing the latest Fed activity as well as the uncertainty in the pace of the growth in the global economy. The worry, I guess, is that after the run-up in domestic equity markets of the past few years we are heading for a cliff and anything negative will push us off. It’s true that since December 2008 the S&P 500 has earned more than 18%, well above long-term averages. Yet, add just the previous three years and this average drops to 9% – so maybe it’s just making up for lost time! In any event it’s uncertainty about the future that drives market prices. Markets respond as the future unfolds.

Bond Markets

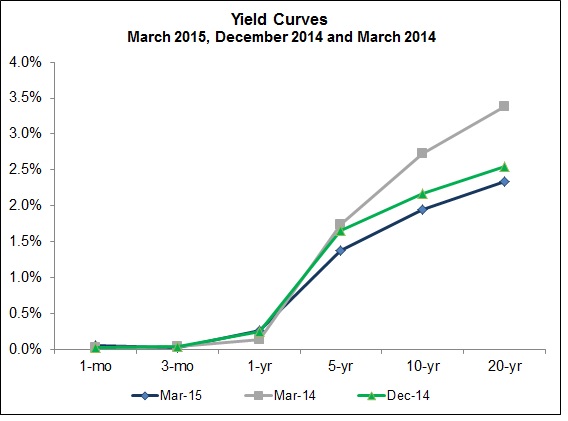

Bond returns, which react inversely to changing yields, were  positive over the past quarter and trailing 12-month periods. These results are consistent with the falling bond yields shown in the accompanying chart. With the domestic economy seemingly doing better, it is well known that the Fed is poised to raise interest rates anywhere from a quarter to three-quarters of a percent. The timing is the only uncertainty. Yet, in the face of expected rate increases, bond yields have continued to fall. I can think of two explanations: (1) temporary market anomalies due to unprecedented Fed activities of recent years, and (2) significantly reduced inflation expectations. I suspect the truth includes both – we’ll have to wait and see.

positive over the past quarter and trailing 12-month periods. These results are consistent with the falling bond yields shown in the accompanying chart. With the domestic economy seemingly doing better, it is well known that the Fed is poised to raise interest rates anywhere from a quarter to three-quarters of a percent. The timing is the only uncertainty. Yet, in the face of expected rate increases, bond yields have continued to fall. I can think of two explanations: (1) temporary market anomalies due to unprecedented Fed activities of recent years, and (2) significantly reduced inflation expectations. I suspect the truth includes both – we’ll have to wait and see.

Expected Inflation

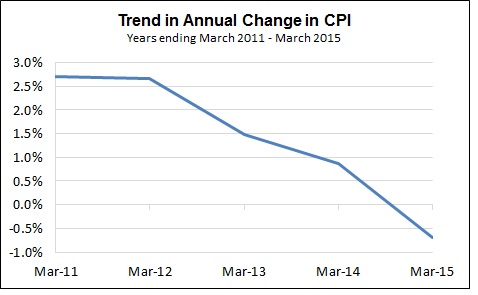

The chart below shows the trend in the annual changes in the Consum er Price Index (CPI) over the past five years. Look how it has fallen to below zero for the most recent period. I suspect this negative number reflects sharply falling energy prices and not necessarily a sign of a general decline in prices across many items (deflation) in the future. Deflation can be a significant drag on economic activity – why spend now if prices are going to be less in the future? – which helps to explain the Fed’s announced goal of keeping inflation at about 2% annually.

er Price Index (CPI) over the past five years. Look how it has fallen to below zero for the most recent period. I suspect this negative number reflects sharply falling energy prices and not necessarily a sign of a general decline in prices across many items (deflation) in the future. Deflation can be a significant drag on economic activity – why spend now if prices are going to be less in the future? – which helps to explain the Fed’s announced goal of keeping inflation at about 2% annually.

Of course, it is expected inflation that is reflected in market prices. However, given today’s negative inflation and bond yields, two conclusions seem reasonable: (1) the Fed is going to have to work hard to meet its inflation target, and (2) future inflation is apt to be less than what we have experienced in the past.

News

As we deal with the daily ups and downs of market averages, it is important to keep in mind that stock prices are determined by the actions of both a buyer and a seller – each has access to the same information. They interpret it differently, but the price that results is where they are both happy. Now, we may think that those who traded last got it all wrong, but there is little evidence of long-term success from betting against the “wisdom of the crowds,” which is reflected in the market price.

While uncertainty abounds, as it always does, it seems like what could impact stock and bond values is pretty well known and, therefore, is part of today’s price. Of course as we go through time, we are going to receive new information (“news”) not only about the eventual outcome of today’s uncertainty, but also about new things to worry about. Some of this new information will be positive, some will be negative; all will be a surprise. The impact of these surprises is the risk we endure, safe in the expectation that over time we will be paid for bearing this risk. That’s how markets work!

If you’re ready to start planning for a brighter financial future, Rockbridge is ready with the advice you need to achieve your goals.