Ready to get started?

If you’re ready to start planning for a brighter financial future, Rockbridge is ready with the advice you need to achieve your goals.

April 10, 2014

All

Myth – n. A fiction or half-truth, especially one that forms part of an ideology. (American Heritage Dictionary)

Dividend paying stocks seem to have attained mythical proportions in recent years as people look for ways to coax income from their investment portfolios.

The idea that dividend paying stocks are somehow superior to other stocks, or an acceptable substitute for low-yielding bonds, is based on many half-truths.

Some say that dividend paying stocks are more conservative and likely to hold their value, so in a down market you can ignore the decline in share price and keep enjoying those dividend payments. That may be half true, but in 2009, 57% of dividend paying companies, across 23 developed markets, reduced their dividends or eliminated them completely while market values were also tanking.

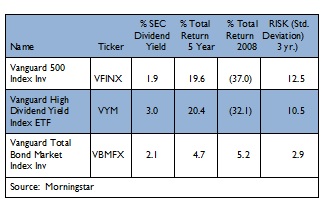

Dividend paying stocks are still subject to stock market risk, which makes them very different from bonds, and well, just like stocks. See the table below which compares a high dividend index fund to the S&P 500 index fund and a total bond market index fund. The first column of numbers shows that the high dividend stocks do indeed pay high dividends, with a current yield even higher than the bond fund.

The second column shows that total returns for stocks (dividends + appreciation = total return) have been far greater than total returns for bonds over recent periods.

The second column shows that total returns for stocks (dividends + appreciation = total return) have been far greater than total returns for bonds over recent periods.

So why own bonds instead of high quality, dividend paying stocks? The answer lies in the last two columns. In 2008 dividend paying stocks displayed their lower-risk characteristics, losing only 32% compared to the S&P at -37%. The bond market gained 5% that year, illustrating the fact that bond returns are not correlated with stock returns, and bonds therefore help diversify a portfolio. The last column shows a measure of risk and illustrates that stocks, even dividend paying stocks, are 3-4 times more volatile than bonds. One way to think about standard deviation is that two thirds of the time, or two years out of three, we can expect returns to fall in a range that is one standard deviation above or below the average. So two thirds of the time bond returns will fall in a range of +/- 2.9% while stock returns will vary +/- 12.5%, and a third of time we can expect returns to come in above or below those ranges.

Bonds diversify a stock portfolio because they are less volatile than stocks and they reduce the correlation of returns among portfolio assets.

As the saying goes, diversification is the only free lunch in investing. Every other potential reward comes with some amount of risk. We are now five years into a bull market, during which we have seen historically low volatility in stocks. Despite the euphoria of recent returns, it is important for successful investors to separate fads and myths from the fundamental principles of long-term investing. Assuming any set of stocks is an acceptable substitute for bonds is likely to lead to unpleasant surprises. Dividend paying stocks are just another unacceptable substitute.

If you’re ready to start planning for a brighter financial future, Rockbridge is ready with the advice you need to achieve your goals.