2013 Year in Review

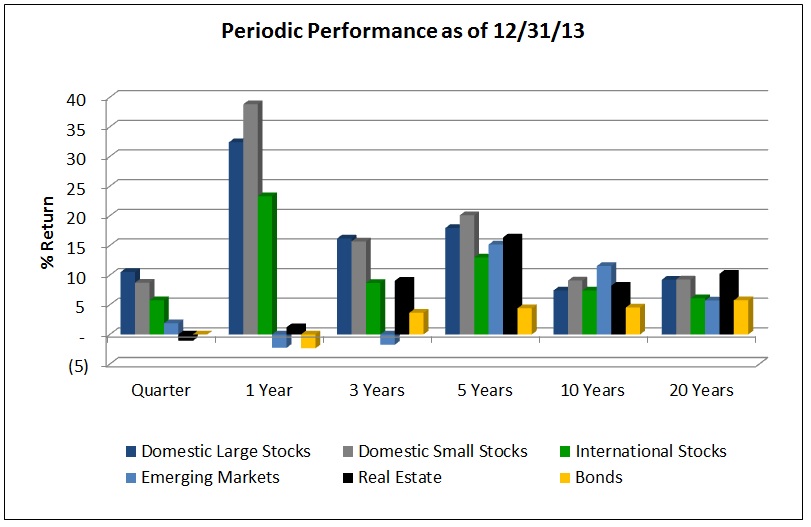

It was a fantastic year overall for the financial markets, cappe d off with the S&P 500 Index closing at an all-time high of 1,848 (up 32.4%). In addition to the domestic stock market, developed international stocks also advanced 23.3%. In contrast, there were a few market segments that lagged for the year. The bond market ended the year down 2.4%, which was the first negative year since 1999 (see “Bonds Continue to Present a Conundrum”). In addition, emerging markets and TIPS both finished the year with negative returns, -2.3% and -8.8% respectively. Finally, REITs were relatively flat compared to recent years returning only 1.2%.

d off with the S&P 500 Index closing at an all-time high of 1,848 (up 32.4%). In addition to the domestic stock market, developed international stocks also advanced 23.3%. In contrast, there were a few market segments that lagged for the year. The bond market ended the year down 2.4%, which was the first negative year since 1999 (see “Bonds Continue to Present a Conundrum”). In addition, emerging markets and TIPS both finished the year with negative returns, -2.3% and -8.8% respectively. Finally, REITs were relatively flat compared to recent years returning only 1.2%.

Consumer Confidence

With the recent run up in the equities market, consumers have turned optimistic about the economy. With this confidence, and the desire for additional yield not currently available in the bond market, some investors are gravitating toward a more aggressive asset allocation. Unfortunately, taking on more investment risk at a market high is not the best investment approach. We strongly believe that maintaining a stable asset allocation will yield the best returns over the long run. Rebalancing at the end of 2013 meant selling US and international stocks and buying additional positions in the bond market.

2014 Outlook – More Uncertainty

As with 2013, there is still a great deal of uncertainty ahead for 2014. Low returns in the bond market are a major challenge that will be exacerbated as interest rates rise. The general consensus is that short-term rates will rise in the future, but the timing is still uncertain. Another major challenge for 2014 is the pace of growth in the economy. While there is positive growth, the rate is below historical averages. This slow growth is also affecting the employment figures. Finally, there is still political uncertainty in Washington which drives a continued high level of market volatility.

Bonds Continue to Present a Conundrum

Yields are low. Rates are likely to rise, sooner or later. When rates rise, the market value of bonds declines, cancelling out the meager interest return, or even creating negative returns as we saw in 2013.

Q: So why invest in bonds?

A: We continue to invest in bonds because they diversify a risky portfolio that includes stocks, and provide a higher expected return than cash, which is the alternative for diversifying stock risk.

Q: With interest rates so low, how much better is the expected return from bonds compared to cash?

A: The current reward for taking bond risk can be observed by looking at the difference, or “spread”, between cash at 0% (Fed Funds rate) and ten-year Treasury bonds now hovering around 3%. By historical standards, that reward is well above average. The spread between Fed Funds and the ten-year Treasury averaged 1.7% over the past 10 years, and averaged only 0.5% over the past 60 years! Similarly, the spread between the two-year Treasury and the ten-year Treasury is now over 2.5%. That spread has not exceeded 2.75% any time in the past 30 years. Everyone expects rates to rise (sooner or later) and that results in historically high rewards for locking in longer maturities on bonds.

Q: So if we do invest in bonds, wouldn’t individual bonds be better, because we can hold them to maturity and ignore changes in market value?

A: Not really, at least not for long-term investors. Ignoring a change in market value does not make it go away. When a bond portfolio is “marked to market” after a rise in interest rates, its current yield is necessarily higher. This is what happens with a bond mutual fund. If an individual investor ignores the change in market value, his current yield remains the same. Over time this difference washes out as bonds mature and are replaced with new bonds with higher yields.

To recap: We continue to invest in bonds because they diversify stock market risk and provide higher expected returns than cash.