Ready to get started?

If you’re ready to start planning for a brighter financial future, Rockbridge is ready with the advice you need to achieve your goals.

January 20, 2015

All

Stock Markets

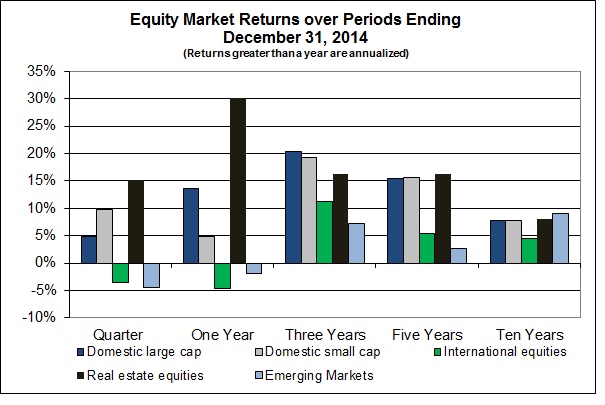

The accompanying chart shows domestic stocks up and international stocks down over the past quarter and one-year periods. Real estate investment trusts (REITs) were up substantially in these same periods. The largest U.S. companies have been especially strong recently and, because these are the stocks followed by the mainstream media, we have the illusion of robust stock markets in 2014. But, it’s a big world and it is important to look beyond our shores to participate in the risks and returns of global markets. Knowing that various markets act differently from one another is important in understanding the investment landscape, especially in recent periods.

Look at the ten-year numbers. Not only are returns more consistent, except for international markets, they are reasonably close to long-term averages. It is not reasonable to expect that international markets will trail other markets over long periods; it only shows that ten years are not necessarily the long run.

Bond Markets

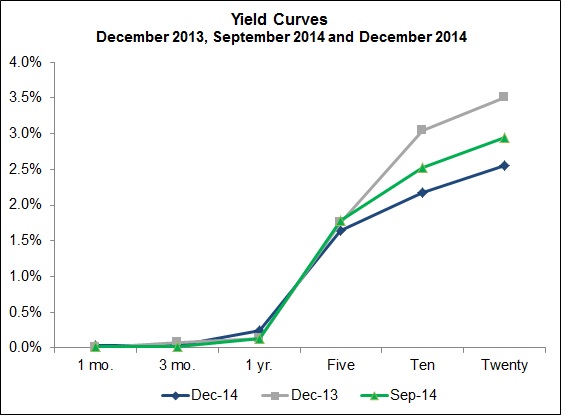

Bonds did quite well as yields declined over the year, even as the Fed began cutting back on its Quantitative Easing programs. Look at the accompanying chart and how yields at the longer end of the curve fell over the past quarter and one-year periods. Declining bond yields are not typically associated with the improving domestic economy that we have been experiencing. This decline seems to reflect a prediction that the Fed will keep short-term rates near zero well into the future. It also seems to reflect the global economic uncertainty, especially in Europe, and the relative safety of U.S. Government bonds.

Some Thoughts on 2015

The Stock Market – If there are no surprises, it is reasonable to expect overall market returns in the neighborhood of 7% after inflation, and in the case of small-cap stocks and international stocks, a little more. Of course, there will be surprises – some positive, others negative – all of which can have a significant effect on returns. Today’s increased volatility paints a picture of more surprises of greater magnitude in 2015. The uncertain effect of falling oil prices on both producing and consuming economies is one unknown that could have a dramatic impact on stock markets around the world.

The Bond Market – What is in store for bond markets in 2015 depends to a great extent on when the Fed raises short-term interest rates. The Fed’s timing is apt to be a surprise. Delay beyond the expected time frame will be positive; sooner will be negative. The current turmoil in the world economies and how the various Central Banks respond will also continue to impact bond yields. Yet, it’s still hard to imagine lower bond yields in 2015.

Wall Street – Things on Wall Street are beginning to look a lot like they did prior to 2008. Profits are up, bonuses are back, and concentration is greater – all from engaging in questionable value-adding activities (this time around it is mergers and acquisitions of large public companies).

Investing Internationally

Diversification means usually owning something you wished you didn’t. This time around international stocks had a terrible year. Yet, investing in this asset class improves a portfolio’s profile of risk and returns. However, to realize the long-term benefits of this diversification, differences in short-term returns must be endured.

The lagging performance of international stocks in recent years has been dramatic and has dragged down past returns such that even twenty-year returns are significantly lower for international stocks (5.4% versus 9.9% for domestic markets). However, market prices reflect the future and there is no reason to expect U.S. markets to continue to outperform other parts of the world. Market forces will attract capital to where returns are expected to be the highest, bidding up prices of outperformers and discounting prices for the laggards. In the long run, risk and return are related. The benefits of diversification (e.g., reduced risk without reduced expected returns) are because short-term returns from different markets are not completely correlated. The lack of correlation between domestic and international markets was certainly clear in 2014.

International markets have rebounded more slowly from the financial crisis than those in the U.S. Some would suggest this disparity could have been predicted. However, investment capital is very mobile and investors everywhere prefer low risk and high return, which is evidence that market participants have been surprised. Above-average returns in domestic markets and below-average returns in international markets cannot be expected to continue. Now, surprises happen randomly. The only way to take advantage of this random activity is to rebalance back to long-term allocations (buy low and sell high) consistently, because risk will be rewarded in the long run.

If you’re ready to start planning for a brighter financial future, Rockbridge is ready with the advice you need to achieve your goals.